are mortgage life insurance worth it

Mortgage Life Insurance is an innovative way to provide life insurance. Some might say it's an over-the-top method, and in many cases, they're correct. However, as stated earlier, many agents utilize this marketing strategy to attract prospective homeowners. They are aware of the requirement for additional life insurance coverage.

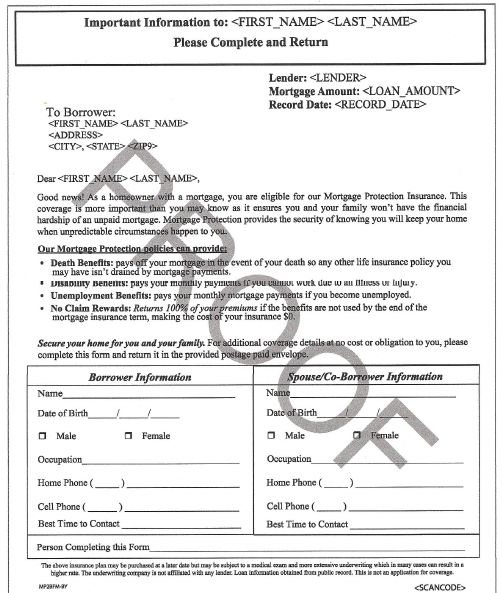

If you just recently purchased a home or refinanced your mortgage, you will likely receive many offers in the mail for "Mortgage Life Protection" or "Mortgage Life Insurance." In this article, we will take a look at the pros and cons of Mortgage Protection Insurance. You can answer the question: Is Mortgage Protection Life Insurance a scam or a smart move?